Can You Roll an 401k Into a Roth Ira

10 Minute Read | November 09, 2021

The Roth IRA and 401(k) are like cousins: They come from the same family of retirement investment accounts, so they have a lot in common. But look close enough, and you'll see how different they are!

Once you understand how they work, you can choose the plan that will help you maximize your savings. And that's not just fancy investing talk. Your choice today could result in thousands—if not millions—of dollars down the road! You need to understand your options so you can be 100% prepared for retirement.

So, what are the major differences between a Roth IRA vs. a 401(k)? And even more importantly: How do you know which one is better for you?

First, let's discuss the main features of each account.

What Is a 401(K)?

A 401(k) is a retirement savings plan that many employers offer. You can invest a percentage of your pay or a specific amount each month. And you make your investments with pretax money, meaning that whatever you invest is taken out of your paycheck before your income is taxed.

We filter out sleazy advisors. See up to five investing pros we trust.

A 401(k) is named after the subsection of the IRS code that talks about retirement plans. (It's athrilling document to read . . . just kidding.) The money you invest can go into several different types of mutual funds, depending on your plan.

Certain businesses don't offer a 401(k) plan, but they might offer something like it:

- 403(b) –This plan is like a 401(k) for tax-exempt organizations like public schools, hospitals or religious groups.

- 457(b) – This plan is offered by state and local governments and some nonprofits.

A huge plus of 401(k), 403(b) and 457(b) plans is that your employer can match your investment up to a certain amount. Matching isn'trequired by the government, so not all employers offer it. If your company offers a 401(k), find out if your employer offers a match so you can make the most of your investing dollars. We're talking aboutfree money, everybody!

And here's some peace of mind: The money you invest isall yours. You can roll over your 401(k) account to an IRA if the company goes under or if you decide to move on.

Advantages of a 401(k)

Let's take a look at some of the main advantages of a 401(k):

- Contribution limit. You can investup to $20,500 a year in a 401(k), 403(b) or inmost 457(b) plans—not including the employer match. If you're 50 or older, you can add an additional $6,500 per year, for a total of $27,000.1

- Employer match. Who doesn't love free money? If your employer offers a match, you should take advantage of it.

- Tax break. You invest in your 401(k) with pretax dollars, lowering your taxable income for that year.

Disadvantages of a 401(k)

While a 401(k) is a great way to save for retirement, here are a few drawbacks to be aware of:

- Fewer options for mutual funds. Your employer hires a third-party administrator to run the company's retirement plan. That administrator determines which mutual funds you can invest in, limiting your options.

- Waiting period. If you're new to a company, you may have to wait a certain length of time to participate in a 401(k) plan.

- Required minimum distributions (RMDs).You can't leave your money in your 401(k) forever. Beginning at age 72, youmust start withdrawing a certain amount of your savings each year, or you'll pay a penalty.2 Also—there are penalties for withdrawing money before age 59 1/2. Either way, Uncle Sam wants his share!

Let's turn to the Roth IRA, and then we'll compare the two.

What Is a Roth IRA?

A Roth IRA (Individual Retirement Arrangement) is a retirement savings account you can open yourself. Unlike a 401(k), you contribute to a Roth IRA withafter-tax money. When you hear the word Roth, thinkhappy—because a Roth IRA allows your savings to grow tax-free . And when you celebrate turning 59 1/2, you can withdraw money from your account tax-free!

An IRA is a great option for people who are self-employed or who work for small businesses that don't offer a 401(k) plan. And if youdo have a 401(k), you could saveextra money and diversify (a $10 word fordon't put all your eggs in one basket) your investments by opening an IRA.

Advantages of a Roth IRA

Here are some advantages a Roth IRA has over a 401(k):

- Tax-free growth. The biggest benefit is the tax break. Since you invest in your Roth IRA with money that's already been taxed, the growth isn't taxed, and you won't pay any taxes when you withdraw your money at retirement.

- More investing options. With a Roth IRA, you don't have a third-party administrator deciding which funds you can invest in, so you can choose any mutual fund you like. But be careful: Always seek good advice when choosing mutual funds, and make sure you fully understand how they work before you invest any money.

- Set up apart from an employer. Unlike a workplace retirement plan, you can open a Roth IRA at any timeas long as you deposit the minimum amount.The amount will vary based on who you open your account with.

- No required minimum distributions (RMDs).With a Roth IRA, you won't be penalized if you leave your money in your account after age 72 as long as you hold the Roth IRA for at least five years.But like the 401(k), you'll be penalized for taking money out of a Roth IRA before age 59 1/2 unless you meet specific requirements.

- The spousal IRA. If you're married but only one of you earns money, you can still open an IRA for the non-working spouse. The spouse who earns money can invest in accounts for both spouses—up to the full amount! A 401(k), on the other hand, can only be opened by someone earning an income.

Disadvantages of a Roth IRA

Just like a 401(k), a Roth IRA has its downsides:

- Contribution limit. You can only invest up to $6,000 in a Roth IRA each year or $7,000 if you're age 50 or older.3 That's a lot less than the 401(k) contribution limit.

- Income limits. If you're single or the head of a household, your modified adjusted gross income (MAGI) has to be less than $125,000 to contribute the full amount to a Roth IRA. If you're married and file your taxes jointly with your spouse, your MAGI must be less than $198,000. If your income is above these limits, the amount you can invest is reduced. And if you make $140,000 or more as a single individual or $208,000 or more as a married couple filing jointly, you're not eligible for a Roth IRA.4 However, the traditional IRA would still be an option.

Roth IRA vs. 401(k): What Are the Major Differences?

Themain differencebetween a Roth IRA and 401(k) is how the two accounts are taxed. With a 401(k), you invest pretax dollars, lowering your taxable income for that year. But with a Roth IRA, you invest after-tax dollars, which means your investments will grow tax-free.

Okay, folks, does anybody else feel like they've been drinking water from a firehose? That was a lot of information! Let's review the main differences between the Roth IRA and the 401(k) so you can easily compare their features:

| Feature | 401(k) | Roth IRA |

| Eligibility | Only available through employer-sponsored programs. May be a waiting period before enrollment. | Must have earned income, but restrictions apply after a certain income based on your filing status. Married couples with only one income earner may open a spousal IRA. |

| Taxes | Investments made with pretax dollars, lowering your taxable income. You'll pay taxes on any money you withdraw in retirement. | Investments are with after-tax dollars, allowing investments to grow tax-free. No taxes on withdrawals in retirement. |

| Contribution Limits | For 2022, $20,500 per year ($27,000 per year for those 50 or older). Additional contributions limits may apply to Highly Compensated Employees (HCEs). | For 2021 and 2022, $6,000 per year ($7,000 per year for those age 50 or older). |

| Employer Contribution | Many employers offer a match based on a percentage of your gross income. | No matching contribution. |

| Required Minimum Distributions (RMDs) | Beginning at 72, you must start taking out a certain amount each year (RMD) to avoid penalties. | No RMDs. The money can sit in your account as long as you live. |

| Investment Menu | Account is controlled by a third-party administrator who handles (and limits) investment options. | A wider variety of investment options and more control over how you invest. |

| Penalties | Penalties for withdrawals before 59 1/2. | Penalties for withdrawals before 59 1/2. |

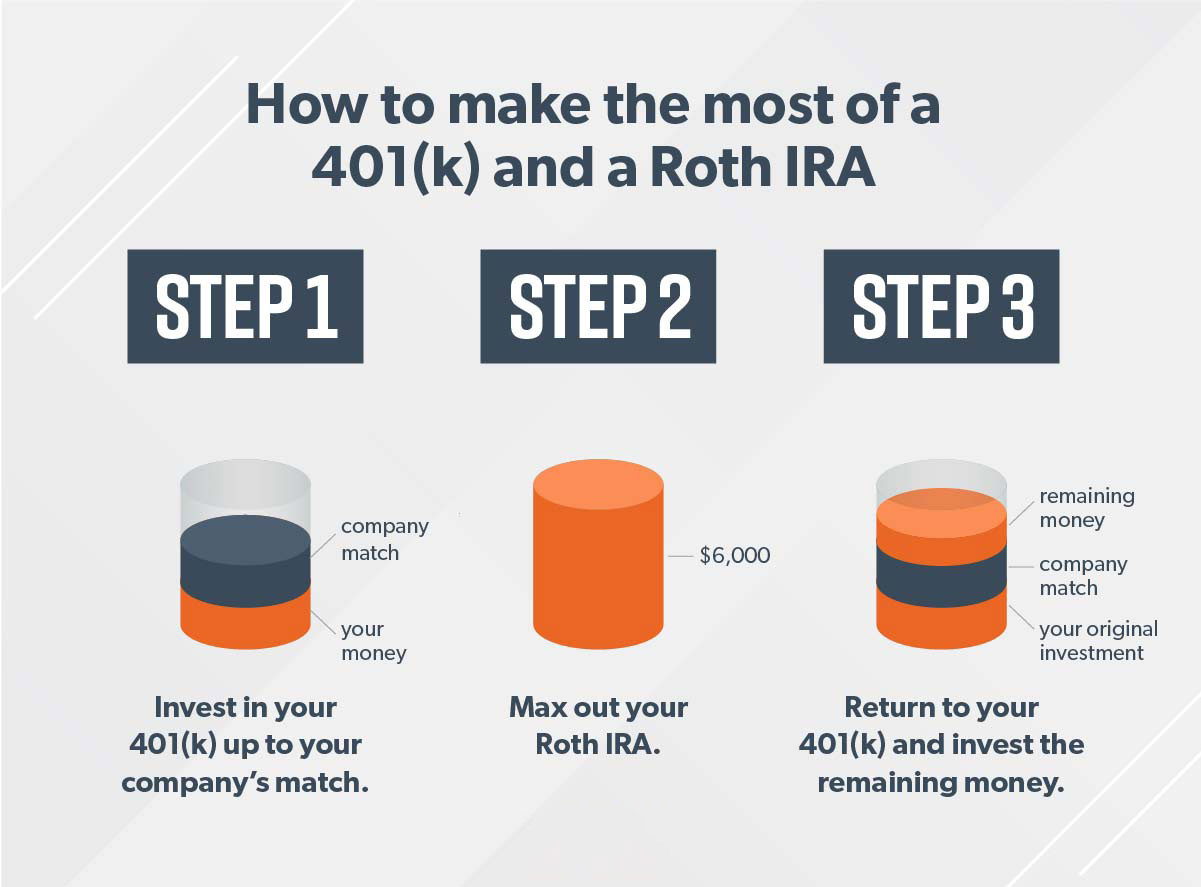

How to Make a 401(k) and Roth IRA Work Together

At this point, you may ask whether you should put your money in a 401(k) or a Roth IRA. The answer is yes .

If you're eligible for a 401(k) and a Roth IRA, the best-case scenario is that you invest inboth accounts (and if you can max them both out—go for it!). That way, you're taking advantage of your employer matchand getting the tax benefits of a Roth IRA.

Here's how that works in three simple steps: Let's say you make $60,000 a year and you're under 50. Your goal is to invest 15%—$9,000 in this case—in retirement.

- You start by investing in your 401(k) up to the match that your company offers. Let's say, in this case, that it's 3% of your gross income ($1,800). You invest $1,800 in your 401(k) to reach the employer match. This leaves you with $7,200 more to invest.

- Then, you max out your Roth IRA. You can only contribute $6,000, so that leaves you with $1,200.

- Return to your 401(k)and invest the remaining $1,200.

Remember, if you're older than 50, there are "catch-up contributions" you can make to max out your Roth IRA at $7,000 and your 401(k) at $26,000.

You may be wondering what you should do if your employer doesn't offer a 401(k) and you've maxed out your Roth IRA for the year. The short answer? You need your money to grow. You can still work with an investment pro to invest in growth stock mutual funds that aren't connected with a retirement account. After you invest your money, leave it alone. Investing is a marathon—not a sprint.

The Best Choice: Work With a Pro

Here's the deal: Investing is worth the hard work. If you don't save and invest now, you won't have anything to live on in retirement. It can be intimidating and complex, but you don't have to do this alone.

Talk with aninvestment professional like our SmartVestor Pros. Get someone on your team who will help you stay focused and chasing your dreams. They can walk you through your 401(k) and Roth IRA contribution options and create a plan for your situation.

Find a SmartVestor Pro in your area!

About the author

Ramsey Solutions

Ramsey Solutions has been committed to helping people regain control of their money, build wealth, grow their leadership skills, and enhance their lives through personal development since 1992. Millions of people have used our financial advice through 22 books (including 12 national bestsellers) published by Ramsey Press, as well as two syndicated radio shows and 10 podcasts, which have over 17 million weekly listeners.

Thank you! Your guide is on its way.

Invest With a Pro Who Gets This Stuff

Invest With a Pro Who Gets This Stuff

Your future is too important for guesswork. Get help from a SmartVestor Pro today.

Find Your Pro

Invest With a Pro Who Gets This Stuff

Your future is too important for guesswork. Get help from a SmartVestor Pro today.

Find Your Pro

Can You Roll an 401k Into a Roth Ira

Source: https://www.ramseysolutions.com/retirement/401k-vs-roth-ira

0 Response to "Can You Roll an 401k Into a Roth Ira"

Post a Comment